SUMMARY

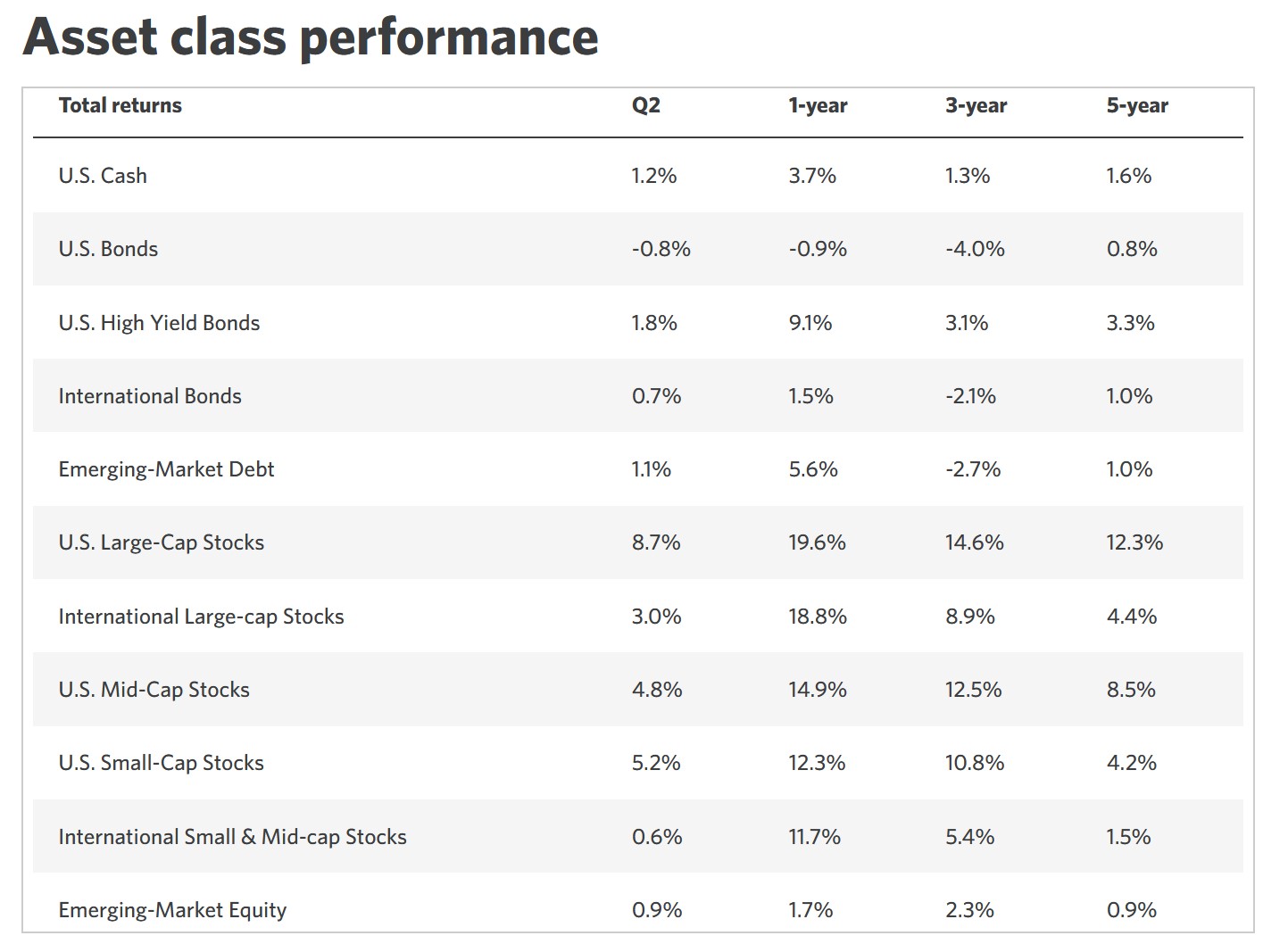

U.S. stocks rose sharply in the second quarter. The Dow Jones Index was up 4% to 34,355 and is up 4.9% year to date. The S&P 500 was up 8.7% to 4,449 and is up 16.9% year to date, mainly on the strength of a handful of stocks (see below). The NASDAQ shot up 13.1% to 13,832, led by AI stocks and is up 32.3% year to date. (The all time high for the Dow was 36,952 on 1/5/22, for the S&P 500 it was 4,818 on 1/4/22 and for the NASDAQ it was 16,212 on 11/22/21.)

U.S. bond yields (moving inversely from bond prices) rose in the second quarter as banking sector concerns subsided and market expectations for the peak fed funds rate increased.

Despite a bounce in natural gas, commodities continued to fall, led by metals and crude oil, as a result of demand concerns regarding the U.S. and China and increasing supply in the energy space. REITS were choppy on dynamic Fed/Market interest rate expectations.

QUARTERLY RECAP

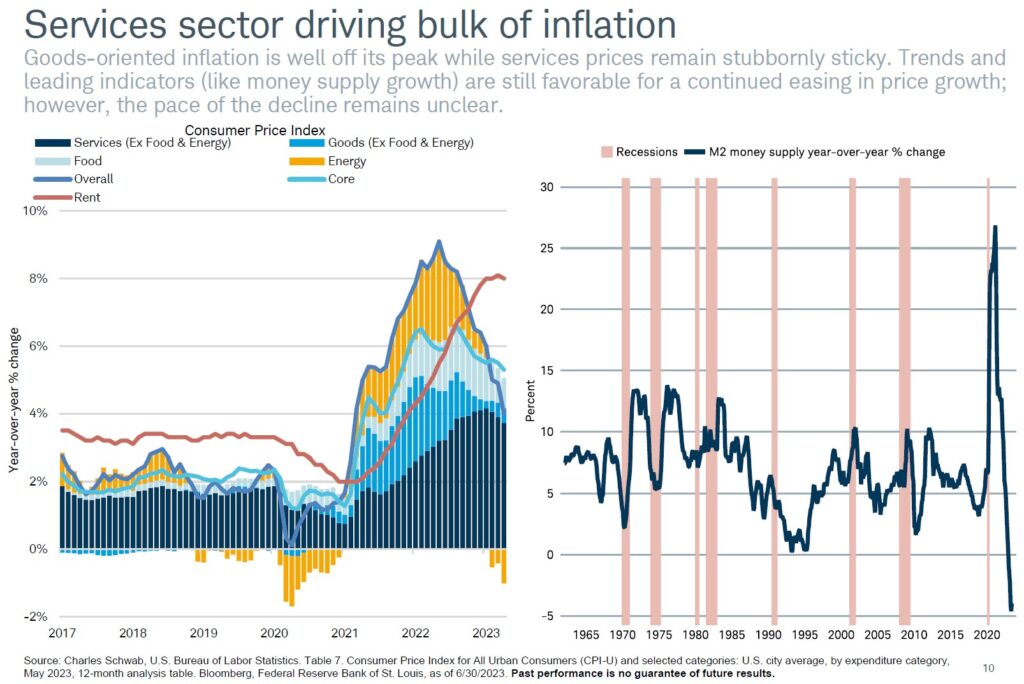

Economy – While concerns about banking stress carried over from the first quarter into the second quarter, key elements of the economy continued to show resilience. Most notably, hiring (as measured by nonfarm payrolls) reaccelerated in the first two months of the quarter. There was an uptick in initial jobless claims, although the increase wasn’t enough to suggest significant weakness (as of now) spreading throughout the entire labor market. Key inflation metrics continued to ease, but those tracked closely by the Fed which exclude food, energy, and housing components are stubbornly sticky, suggesting the Fed still has progress to make in its fight to get to a 2% inflation target.

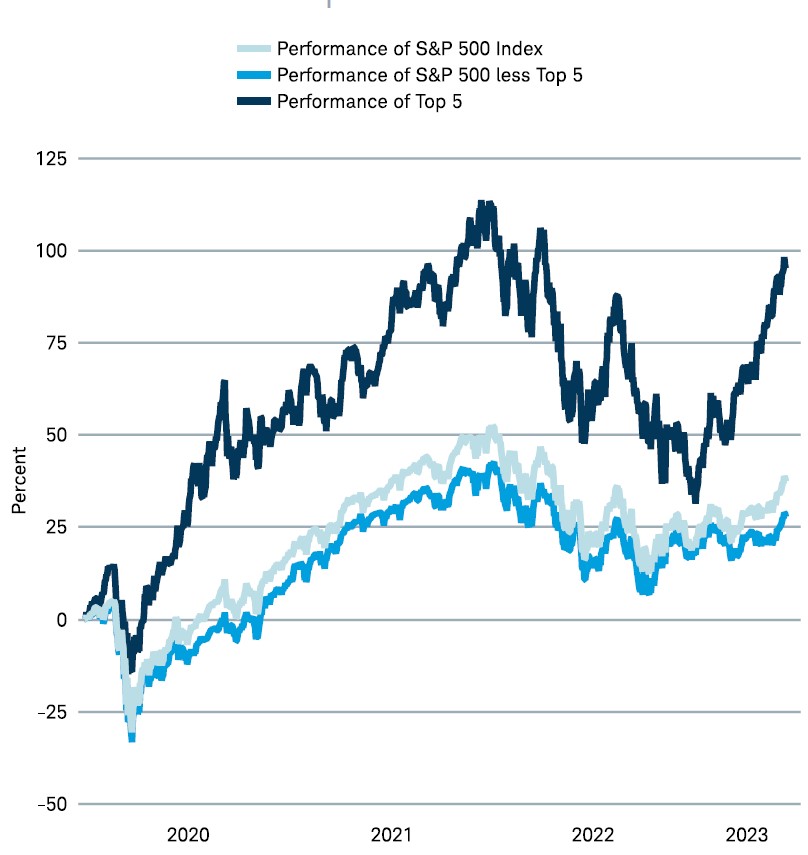

Equities – U.S. stocks continued to climb throughout the quarter, boosted heavily by large cap names. The market remained significantly divided as investors continued to leavie small caps and cyclical segments of the market behind (likely a symptom of the banking stress in March). As a result, concentration risk crept ever higher. The increasing risk has been a lack of participation from the “average stock,” or the rest of the market, excluding the mega cap names.

Income – U.S. Treasury yields climbed higher in the second quarter as the Federal Reserve continued to raise its benchmark interest rate. After hiking in May and holding rates steady in June, projections from the Federal Reserve suggested that more rate hikes may be needed this year to bring inflation down. According to the fed funds futures market, the peak rate may remain high into next year. The yield curve further inverted as short-term yields rose more than long term yields; the 10 year Treasury yield continues to trade below the fed funds rate as the market prices in future rate cuts.

Commodities – Demand worries in the world’s two largest economies of the U.S. and China weighed broadly on the commodity complex, notably metals and energy. The markets grappled with whether the Fed’s hyper aggressive monetary policy tightening will pull the U.S. economy already bogged down by slowing goods consumption into a recession. Meanwhile, China’s disappointing economic recovery and still struggling property sector weighed on commodities. However, natural gas rebounded sharply on the threat of further European supply disruptions, and hot weather driven global demand surges, while Europe’s heating season loomed. A stable U.S. dollar likely limited some of the volatility.