We all want a secure financial future. We want to know that our retirement funds are invested well, and that they will provide for a comfortable life throughout the duration of our retirement. This means we must periodically review performance against plans, changing assumptions, and what obstacles might stand in the way.

Today, we’re going to take a look at the long-revered 4 Percent Rule, to explore whether it still holds true today given the current state of the bond market, and what you can do to best ensure your nest egg is ready for your retirement years.

The 4 Percent Rule

The 4 Percent Rule

You may already be familiar with the 4 Percent Rule, which made ripples when published in the 1990s, and is still widely used as a starting point today. The 4 Percent Rule itself is a withdrawal rate suggestion tool for retirement: that a retiree can withdraw 4 percent of their savings each year and still have their funds last for at least thirty years.

The 4 Percent Rule came from an extensive study published in 1994 by financial advisor, William Bengen, who combed through fifty years of data on stock and bond returns. Bengen found that, tested against even the worst historical market conditions, a 4 percent rate of withdrawal would go the distance for thirty years—one percent less than the previously accepted standard of 5% annual withdrawal.

Part of a Traditional Retirement Portfolio

One drawback to the 4 Percent Rule is that it assumes a very specific blend of investments, which may or may not reflect your personal financial realities. The rule assumes that retirement funds are invested in a combination of stocks for growth, and relatively safer bonds, which have largely stood the test of time.

The reason for this blend is because while growth stocks carry higher rates of return, they also come with increased risk of volatility, and as the saying goes, the bigger the risk, the bigger the reward.

While stocks in a healthy market traditionally yield higher rates of return than bonds, they are by nature unpredictable, and an economic downturn could set a portfolio back by years. Tough times on Wall Street could spell disaster for a portfolio heavily relying on high-risk stocks, and thus most retirement portfolios include a large holding of bonds as an element of risk management.

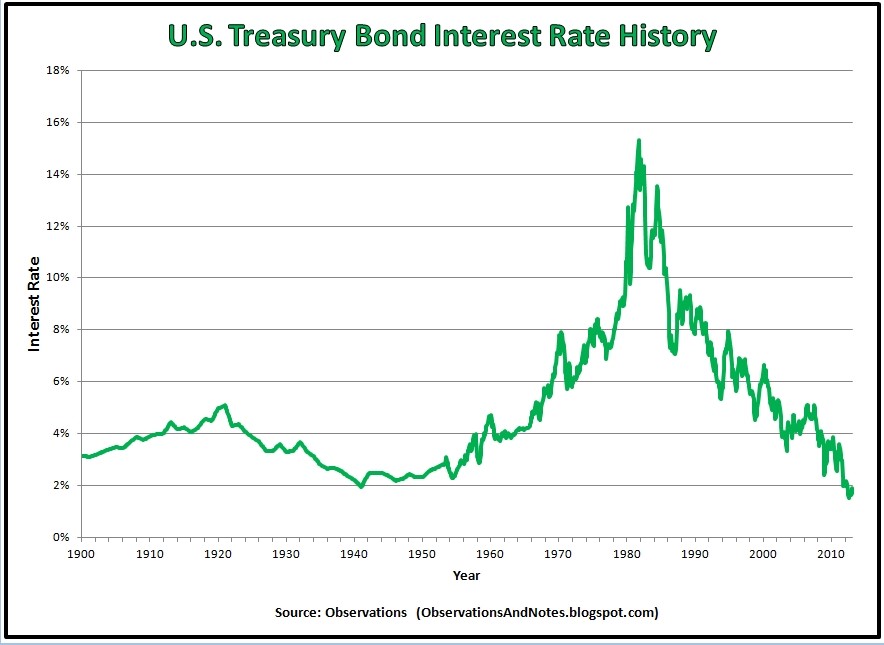

The 4 Percent Rule itself assumes a portfolio allocation of roughly 60% safe bond holdings and 40% stocks, but with historically low interest rates today, two questions we hear often are: “Does the 4 Percent Rule still apply?” and “How does it hold up in today’s market?”

Still Relevant?

The short answer is that it’s complicated. As Bengen himself observed in 2012 when he reexamined the study, the 4 Percent Rule generally still holds true. However, he also noted that the future is unpredictable, and that no fund or investment strategy is perfect, and as such, no one rule of thumb alone can guarantee your retirement fund will be able to go the distance.

The traditional blended combination of bonds and growth stocks that the 4 Percent Rule relies upon was established in the 1980s, when bond yields were not just consistently strong, but booming. With current bond yields today averaging between 2-3 percent and with low interest rates, as compared to the 1980,s the yields on the bonds are frankly, well, terrible.

Because of low yields on bonds (which will continue for the foreseeable future), it is more difficult to rely on the kind of year to year growth of a retirement account started today, versus twenty years ago. Today, the safer, less volatile returns from a traditional investment portfolio might not meet your savings needs or goals. For instance, if you start saving late, or know you will need to make a large withdrawal from your fund for a large purchase early in your retirement, your account and savings plan might be drastically affected.

Is the 4 Percent Rule Right for Me?

The truth is that it’s difficult to say—every retiree’s financial situation is different, and there’s no perfect fit investment model that will work for everybody. It would be like trying to make a one-size fits all suit: it just doesn’t work or look good on anyone. There’s a reason why we have things tailored, and the same logic applies to your savings.

If you have a more aggressive investment portfolio now, depending on how the markets perform, you might end up needing to make withdrawals lower than 4 percent in your early retirement, or on the flipside, if your portfolio is booming, you might be able to safely withdraw more than the traditionally allotted 4 percent!

The future is unpredictable, and markets will inevitably continue to go through periods of stability and volatility, and even in the most stable of markets, economic crisis could be lurking around the corner. As such, it’s best to continually monitor your investment and consult your financial advisor as to what strategy makes the most sense for you today, and tomorrow.

Contact us for a review of your portfolio to ensure you will have a secure financial future.